Q1 2023 Cirrus Newsletter

Aerista is widely known as having the most robust data of Cirrus pre-owned prices. One of the benefits of cultivating this data is that it allows us to pontificate on future market conditions with some degree of confidence. Of course, we often get it completely wrong, but it’s always a fun exercise to try to predict where the Cirrus market is headed. So here’s our take…

The price hikes of 2021-2022 have abated and list prices have fallen from their peaks. Deals are now typically struck at a small discount to list price – a condition that was normal prior to Covid, but one we had not seen for 2+ years! However, our assessment is that prices will not return to pre-Covid levels. Inflation and a prevailing balance between supply and demand will keep prices from falling, so those of you hoping the bottom would drop out so you could steal your next Cirrus may be waiting a long time.

Inflation

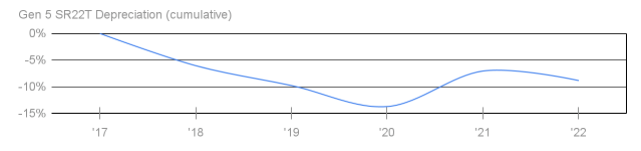

Remember the ‘80s? Big hair, Cabbage Patch dolls and high inflation? Thankfully, only inflation has returned and we analyze its impact below. Our methodology is to calculate REAL depreciation rates by subtracting U.S. CPI from the change in average closing price for that year. We use the G5 Turbo segment because it represents the market very well, with no one-off adjustments that would tend to skew prices, such as CAPS repacks or engine overhauls.

Before Covid, real annual depreciation hovered near 5%. Though Covid demand brought price appreciation in ‘21, we believe the long-term effect was to raise prices to a new base level rather than change the slope of the depreciation curve. We expect a return to real depreciation of 5%. With the economy generating about 6% inflation, this means headline/nominal price levels in the market should be relatively flat.

Resupply, not oversupply

The balanced supply/demand picture will also support flat prices. Though supply of units-for-sale did increase 3-fold from its low of about 80 units in Dec ‘21, it has very much stabilized, with supply hovering in the low-200s. At this level, supply is still below the historic peaks and, of course, is further below those peaks as a percentage of fleet, since Cirrus continues to deliver hundreds of new units each year. Equally important, our transaction data shows that demand kept pace with supply once the restocking reached this low-200s level in ‘22. This steady demand shows no signs of abating, even in an environment of higher borrowing costs. So, not only will inflation generate support for nominal prices, continued demand will put upward pressure on real prices.

Holdouts

All that said, some sellers have been subject to “recency bias”, believing control of the market remains in sellers’ hands. As a result, a few specific segments of the market (G3 TN with Avidyne and G3 SR22 with Garmin Perspective, for example) have not yet fully adjusted to the reality of a balanced marketplace. Prices in these segments will likely move south due to downward pressure from higher-value segments that have already adjusted to the post-peak period.

In short – while we will likely see short-term price declines in a few segments, the rest of the market will be stable with a healthy amount of supply being met by continued robust demand and nominal prices being supported by external inflationary pressure.

We hope you find the discussion useful. If you’d like to connect directly, we’d love to hear from you. As always, we appreciate your continued support as clients and friends. Thanks for making Aerista the largest Cirrus broker in the world.