Q1 2026 Cirrus SF50 Market Update

Cirrus finally pulled the curtain back on the G3 last week. The rumors were loud, expectations were high, and the results were evolutionary, not revolutionary.

The upgrades are primarily software-driven. CPDLC (rebranded as ATC Datalink), meaningful avionics refinement, the AC vent door upgrade, removal of the center console, and legitimate seating for six adults were all smart, well-received changes. Useful? Absolutely. Game-changing? No.

The elephant in the room was Starlink. Buyers were expecting it. That said, it is coming, and once it does, legacy connectivity is effectively dead. GoGo is living on borrowed time. I am short this stock.

Despite the measured upgrades, Cirrus booked well over 20 new orders almost immediately. That tells you everything you need to know about brand gravity and the depth of the SF50 buyer pool.

G1: Quietly Stable, Boring in a Good Way

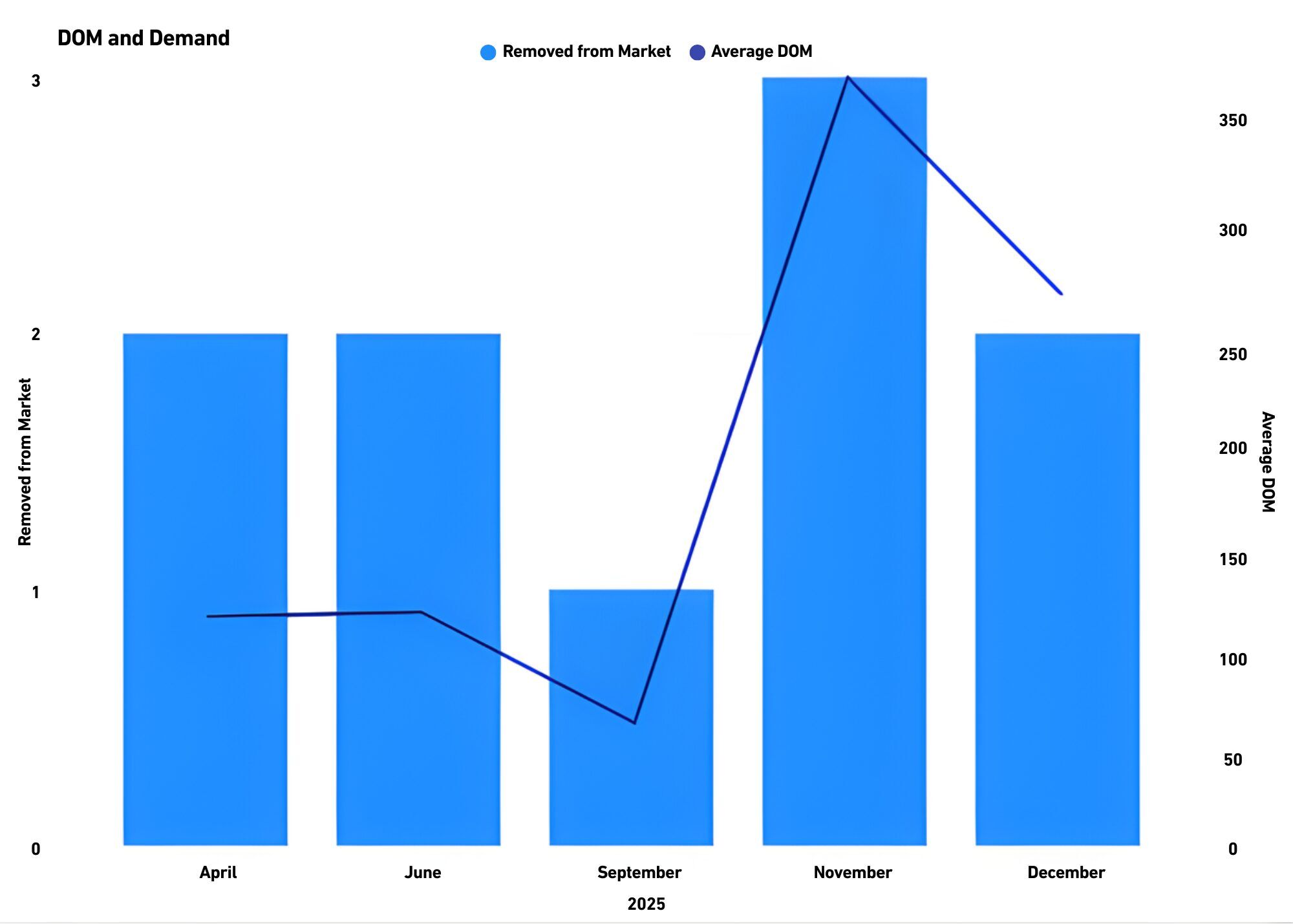

In 2025, 10 of the 88 G1 SF50s traded; about 11% of the fleet. That’s healthy liquidity for a jet at this stage of its life cycle. JetStream remaining continues to cap pricing, and the market spoke clearly: nothing traded above $1.9M. Today, the top ask sits at $1.825M.

Buyers and sellers are meeting in the middle. Yes, average days on market topped 200, but that number is distorted by a few “hope pricing” aircraft. Median days on market was a very reasonable 140. Translation: price it right and it moves.

Supply is thin at five aircraft, and modest depreciation, low single digits, is the most likely path. Some owners may flirt with dropping JetStream and going independent, especially post-2,000-hour hot section.

G2: The Market’s Favorite Child

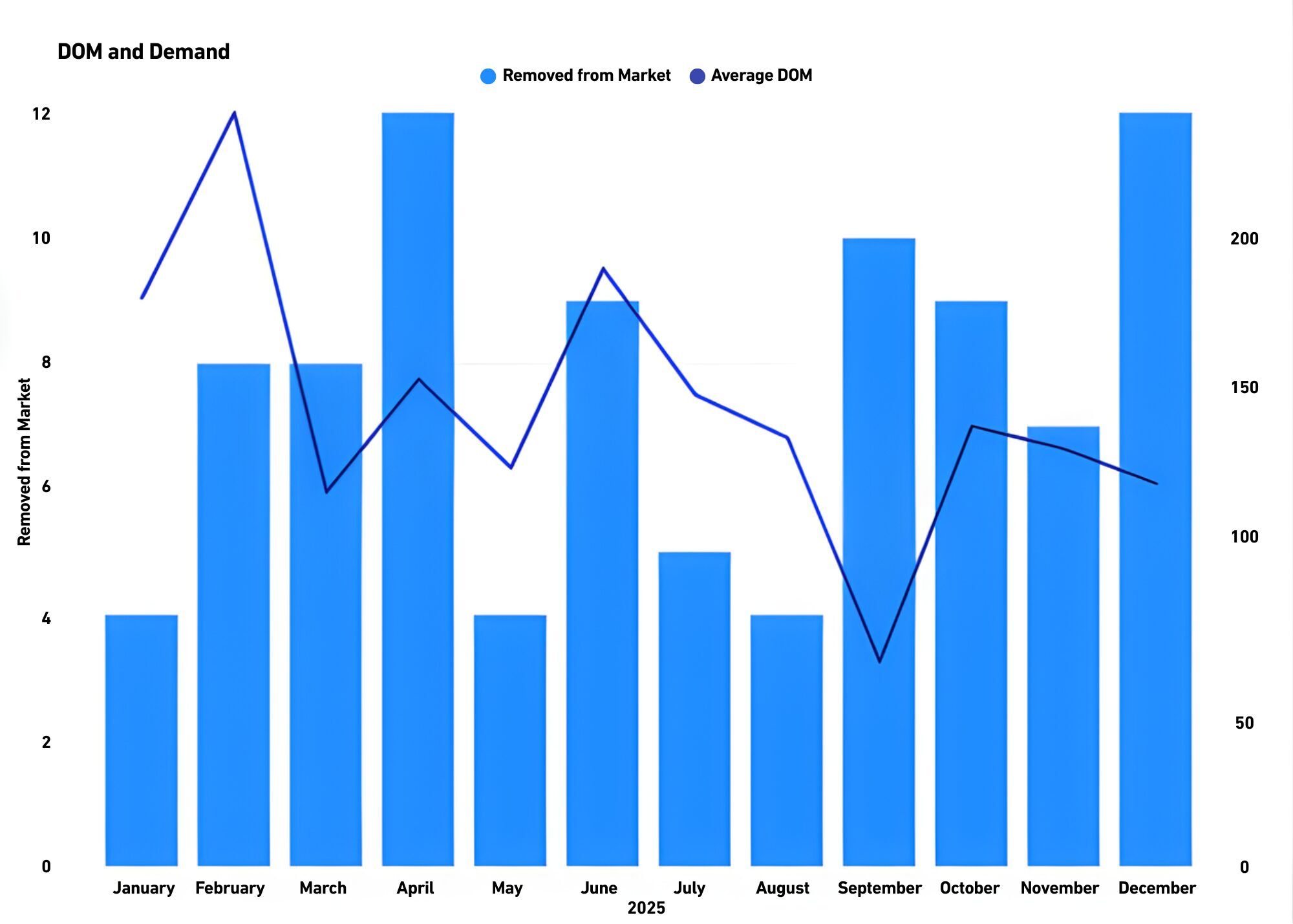

In 2025, roughly 9% of the G2 fleet traded (74 of 791 aircraft). Of those, 53 were G2+ variants. That alone tells the story.

Standard G2s averaged 237 days on market (169 median). G2+ aircraft? Ninety-one days. Buyers have voted, and the ballot was unanimous.

Here’s the hard truth: pricing your G2 is not a creative exercise. Aerista has the data. You can disagree with it, but the market won’t.

The pricing trend is down, but the hierarchy is clear. Clean, late-model G2+ aircraft, no stories, strong JetStream, 2023 or newer, still trade north of $3M. Earlier G2+ aircraft and standard G2s, particularly with lower serial numbers and thinning JetStream, start with a “2.” Features, hours, JetStream, Arrivée, and serial number all matter—but pretending otherwise just extends days on market.

The Question Everyone’s Avoiding

As the fleet pushes past 1,000 units and Cirrus continues producing north of 100 jets annually, we have to ask the uncomfortable question: does the market really absorb 200 SF50s per year when you combine new production and pre-owned supply?

If pre-owned inventory continues to represent ~10% of the fleet, something has to give. Either pricing adjusts downward to clear volume, or late-model aircraft remain the only liquidity while the rest stagnate.

Final Take: G3 Won’t Break the Market

The G3 does not blow a hole in existing SF50 values. At the upper $3M’s, it lives in a different psychological and financial category. G2 depreciation will be driven by supply and Cirrus’ ability to convert SR owners into jet buyers.

The winners will be late-model, well-optioned aircraft priced in reality. The losers will be sellers anchored to yesterday’s comps.

The market always tells the truth.

Warm Regards,

Luke Lysen

Director of Vision Jet Sales